19 March 2025

Alpha Group International plc

("Alpha" or the "Group")

Full Year Results

for the year ended 31 December 2024

Alpha Group International plc, a global provider of high-tech, high-touch financial solutions to businesses is pleased to announce its audited Full Year Results for the year ended 31 December 2024.

Highlights FY 2024

Group Highlights

- Group revenue increased 23% to £135.6m (2023: £110.4m) and increased organically (excluding Cobase1) by 20% to £132.7m (2023: £110.2m)

- Private Markets (formerly "Institutional") revenue increased 20% to £69.0m (2023: £57.4m)

- Corporate revenue increased 21% to £63.8m (2023: £52.8m)

- Cobase revenue increased to £2.9m (2023: £0.2m2)

- Total income, including Net Treasury Income, increased 19% to £220.9m (2023: £186.0m)

- Profit before tax increased 6% to £123.1m (2023: £115.9m)

- Underlying3 profit before tax grew 10% to £47.4m (2023: £43.0m)

- Underlying3 profit before tax margins of 35% (2023: 39%), and excluding Cobase 37% (2023: 39%)

- Client balances from Accounts & Payments solution (formerly "Alternative Banking" solution) increased by 10% to £2.3bn in Q4 (2023 Q4: £2.1bn)

- Net treasury income from interest on client balances, NTI - client funds, increased by 14% to £84.0m (2023: £73.7m)

- Adjusted net cash4 increasing by £38.7m to £217.5m (2023: £178.8m) reflecting our strong cash generation and debt-free position (and on a statutory basis increasing by £55m to £252.5m)

- Basic earnings per share up 5% to 215.7p (2023: 206.2p), and underlying basic earnings per share up 13% to 86.4p (2023: 76.7p)

- Final dividend of 14.0 pence per share, payable on 23 May 2025 to shareholders on the register at 25 April 2025, making a total final dividend for 2024 of 18.2 pence per share (2024: 16.0p)

- Inclusion in the FTSE 250 index in June 2024, following a successful listing on the Premium Segment of the Main Market in May 2024

- Appointment of Dame Jayne-Anne Gadhia to the Board as Chair

- Clive Kahn succeeded Morgan Tillbrook as Chief Executive Officer on 1 January 2025

- Trading momentum in H2 2024 has continued into the year to date, and we remain confident in the outlook for FY25 and beyond

- Change of division name from "Institutional" to "Private Markets" (aka "Private Capital Markets") in order to improve understanding of our target market both internally and externally with clients

1 Financial Transaction Services B.V. trading as Cobase.

2 Cobase was acquired on 1 December 2023, and during the month generated revenue of £0.2m, EBITDA of £0.0m, and a PBT loss of £0.2m.

3 Underlying excludes the impact of non-cash shared-based payments expense, net treasury income on client balances, one-off listing-related and M&A costs.

4 Excluding collateral received from clients, collateral paid to banking counterparties, early settlement of trades and the unrealised mark-to-market profit or loss from client swaps and rolls.

Outlook

The Group's positive trading momentum in H2 2024 has continued into 2025, which combined with the increasing benefits of our investments to date, means we remain confident in the outlook for FY25 and beyond.

We remain very excited to see the progress of our Corporate overseas offices and fully believe each has significant potential to scale and recreate the successes of our UK team, which has itself had a strong start to the year. At the same time, our Private Markets division now has four highly compelling product offerings, each still scratching the surface of its addressable market. This focus on innovation and diversification has subsequently enabled it to deliver strong underlying growth, even in a suppressed market, while also generating significant levels of interest income. Cobase, meanwhile, continues to impress, and we are confident it will make increasingly significant contributions to the Group as time goes on.

Enquiries:

| Alpha Group International plc Clive Kahn, CEO Tim Powell, CFO | Via Alma Strategic Communications

|

|

Alma Strategic Communications (Financial Public Relations) Josh Royston Andy Bryant Kinvara Verdon Louisa El-Ahwal |

+44 (0) 20 3405 0205 |

Notes to editors

Alpha is a global provider of high-tech, high-touch financial solutions to corporate and private market organisations. Working with clients across 50+ countries, we blend intelligent human capabilities with new technologies to provide an enhanced alternative to traditional banking services, with solutions covering: FX risk management, global accounts, mass payments, fund finance, and cash management.

Key to our success is our team - over 500 people based across eleven global offices, brought together by a high-performance culture and a partnership structure that empowers them to act as owners of our business.

Despite being an established business listed on the London Stock Exchange, we remain relentlessly focused on maintaining the same level of operational agility and client focus we had when we first started in 2009. This dynamic, combined with the passion of our people, has enabled us to make a substantial and enduring difference to our clients, and deliver a growth story to match.

Chief Executive's Statement

Introduction

At the time of drafting this report, I have completed two months as CEO of Alpha and spent a total of four months as an executive director, enough time to assess the main merits and de-merits of an organisation, and to develop views on the strategy required. This assessment was also helped by my previous eight years as Chairman of the Group. During this time as Chair, I was continually impressed by the quality of Alpha's offering, the calibre of the Alpha management team and the scale of the future opportunities in front of them. Following my time working even more closely within the business, that admiration has only deepened. It is even clearer than before that Alpha's founder, Morgan Tillbrook, who I have the honour to succeed, has created a remarkable business based on a tremendous culture and admirable values. I feel extremely fortunate to have inherited a strong foundation of talented people and a business offering with exceptional potential. Therefore, I have resisted the natural tendency of incoming CEOs to establish their authority by instituting major change. Strategically, little needs to be changed; my primary objective is to help Alpha fulfil its growth potential through continued focus on those factors that drove our success in the past, plus thoughtful, incremental value-adding adjustments rather than major overhauls.

Alpha's strategy remains focused on sustained top-line growth across our three divisions, driven by continued investment that improves the quality and effectiveness of our customer offerings. This organic growth strategy requires the correct balance between investing in systems and people to drive future revenue growth, whilst ensuring that we continue to achieve meaningful growth in the current year. We strive to prioritise quality, increased competitiveness, and efficiency to ensure that every investment drives meaningful value. We will continue to recruit, coach, and inspire a motivated team, upholding the high-performing but humble Alpha culture that has defined the past growth of our business. Alpha is built on exceptional talent, and I have no doubt that together, we will continue to deliver outstanding results. To strengthen alignment across our divisions, I have also established an Executive Committee which is also designed to enhance collaboration, accelerate decision-making and foster a shared vision. The table below shows Alpha's Executive Committee members.

| Name | Role | Year started with Alpha |

| Clive Kahn | Chief Executive Officer | 2016 |

| Tim Powell | Chief Financial Officer | 2022 |

| Tim Butters | Chief Risk Officer | 2019 |

| Alex Howorth | CEO, Corporate | 2014 |

| Sam Marsh | CEO, Private Markets | 2018 |

| David Christie | COO, Private Markets | 2024 |

| Jorge Schafraad | CEO, Cobase | 2023 |

| Matt Knowles | Strategic Advisor | 2018 |

The impressive top-line growth reflected in our 2024 financial performance is driven by initial returns on the investments made over the last three years to improve our customer offering and market coverage. I am excited by the number of product and market opportunities, the majority of which remain in relatively nascent stages, and I am confident in the scale of untapped demand for our products and services and our ability to execute effectively and deliver sustainable growth for all stakeholders. I believe the future belongs to companies that think smart, move fast and execute with precision. My role is focused on ensuring that Alpha masters these attributes and is therefore built to win.

Reporting

In line with the Group's decentralised structure, as previously set out, the Group now reports its performance against its two markets: the Corporate market and the Private Markets (previously "Institutional"). We also continue to separate out the performance of our recent acquisition, Cobase. This move from a product-centric reporting focus to a client-centric reporting focus was undertaken to align with Alpha's revised organisational structure. Our Institutional division has also been renamed to our Private Markets division, in order to better reflect the types of clients that we serve. Additionally, our "alternative banking" product now becomes our "accounts & payments" product. We have changed this label as we believe that the whole of Alpha's Private Markets offering can be categorised as a "banking alternative", whilst "accounts and payments" is a more specific description of the individual products being provided in this segment.

The next chapter of growth

Alpha's growth capabilities derive from over a decade of continuous investment, and are further driven by significant opportunities for expansion, spanning geographies, industries, product lines, and business cycles. Our Alpha teams continue to work closely to identify and develop new products that address emerging client needs and market demands. Our strong, long-standing client relationships with C-suite decision-makers of some of the world's most respected companies have established Alpha as a leading banking alternative and expert in financial risk management globally. All the above factors combine to produce a substantial runway for future growth.

The resilience of Alpha's performance is aided by an increasingly diverse portfolio of products, client types and geographies, reducing exposure to specific market cycles. This diversified approach also ensures we have the market reach, expertise and talent to capitalise on a wide range of new opportunities, helping to deliver sustainable, long-term success.

We will continue to analyse and manage risk, balanced with commercial opportunity. In 2023 Alpha (and our clients) had to quickly adapt to a new higher interest rate environment. Mindful of this, we chose to reduce our credit appetite in these years, which prevented us from working with some existing clients, whilst reducing the pool of new clients we were willing to work with. However, more than a year on, our teams have significantly more insight into clients' business models and end markets within this environment, allowing them to make more informed client credit decisions, increasing our appetite in some areas, without compromising on our standards.

Corporate

Highlights

· Revenue growth of 21% to £63.8m (2023: £52.8m)

· Client numbers increased 16% to 974 (2023: 838)

· Average revenue per client increased by 12%

· Headcount increased to 199, 65% of which were Front Office (2023: 171, 59% of which were Front Office)

· Underlying profit before tax margin1 of 49% (2023: 47%) as a result of increasing operational gearing and front office productivity

1 The Group does not report a statutory profit before tax measure for its divisions, therefore no statutory comparator is presented.

About

Alpha's Corporate division operates from its own UK HQ (consisting of sales and operations), and six additional international sales offices in the Netherlands, Spain, Italy, Germany, Australia and Canada.

This increasing global coverage allows Alpha to provide a 24-hour financial risk management service to our client base, driven by native speakers in every office. Our risk management offerings seek to protect our clients against volatility in FX and interest rates. We have also begun helping some clients with their exposures to changes in lower-volatility commodity prices, primarily fuel. Revenues are derived primarily from the provision of FX risk management services to corporates across more than 50 countries.

Business Environment

Corporate macroeconomic conditions were largely unchanged from the previous year, with clients continuing to face challenges such as high borrowing costs, reduced cash flow, and limited access to credit. However, we observed a gradual normalisation of financial forecasting and risk hedging in the second half of 2024, as corporates acclimatised to this new reality and felt more prepared to plan for the future.

Performance

I am pleased to report a strong performance for 2024 in our Corporate division, particularly given the challenging conditions. Overall, the division grew revenues by 21% to £64m (2023: £53m), with client numbers increasing 16% to 974 (2023: 838). Average revenue per client grew 12%, reflecting our continued ability to work with larger businesses, as well as increase our wallet share with existing clients as we grow. The underlying profit before tax margin increased from 47% to 49%, reflecting the improved operational gearing filtering through from our overseas offices, as these earlier investments begin to scale.

Delivering such growth is a testament to the strength of our offering in these markets, the quality of talent we have available, and the fruits of our investments, both in London and overseas).

As planned, we made a significant investment into our front office operations in 2024, growing our headcount by 28% during the year to 129 people (2023: 101) across all seven of our Corporate offices.

As we expand our Front office headcount, productivity remains a key focus for us. We measure this by comparing the total cumulative tenure of our front office teams against our revenues.

The widening gap between revenue and cumulative years of experience shown above illustrates that we have increased productivity levels, despite both the market headwinds and experienced salespeople moving into roles focused on leading international expansion and/or the growth and development of our front office teams. When excluding new joiners, whose contribution in their first year is naturally lower than more seasoned colleagues, the growth in productivity is even more pronounced.

We believe the increase in productivity ultimately stems from the growth in our capabilities, cash position, reputation, experience and training over the years. In short - our proposition has never been more compelling and our people have never been better equipped to sell it.

Our Corporate London office delivered a return to growth in FY24, reporting revenues up 7% to £36.6m (2023: £34.0m) and an increasing momentum in H2 with revenue up 9% against the first half. Following a decline in revenues in 2023, our growth was driven by new talent and investments in the team, having previously been impacted by the necessary exporting of talent to launch the overseas offices in the prior years. The 2024 Corporate performance demonstrates our ability to regrow the Corporate London team, whilst maintaining our high standards for talent and cultural fit, positioning London more strongly than ever to continue driving growth.

Having invested significantly into our overseas offices over the past few years, we are now seeing a real return on our initial investments, with the businesses beginning to scale. It is important to note that London now represents 57% of our Corporate revenues compared to 64% last year, reflecting the diversification of our revenues and the increasing value of our overseas offices as a contributor to the Group. Indeed, overseas offices reported revenue growth of 44% collectively in 2024, with excellent contributions from all offices, except Canada, which was flat. As previously reported, we took the decision to change the leadership within our Canada office at the back end of 2023. Encouragingly, revenue performance in the second half of 2024 was stronger than the first and we will look to support its continued growth into 2025.

The strong foundations of Alpha's model and culture, as well as highly knowledgeable and incentivised management teams based across all our overseas offices, fuels confidence that these offices can, over time, scale to mirror the success of our Corporate London operation.

Corporate Growth Strategy

This year will see continued investment across our Corporate division to drive further sustainable growth, while not sacrificing our unwavering focus on our high-quality, client-centric service. We will expand our front-office headcount and invest in our technology to produce further improvements in the quality and efficiency of service to our Corporate clients. This will include improving integration and connectivity into their systems via APIs, which strengthens our relationships.

Above all else, we will continue to uphold Alpha's reputation for integrity by always acting in the long-term interests of our clients. In an industry often driven by short-term sales targets, and where clients frequently fall victim to poor advice, having a provider that prioritises their interests above all else - even if it means walking away from a deal - is a real differentiator for Alpha, and a rare quality that is increasingly recognised and appreciated by the market.

Private Markets Division (formerly "Institutional")

· Revenue increased by c. 20% to c. £69.0m (2023: £57.4m)

· Account numbers increased 10% to 7,103 (2023: 6,467)

· Risk management client numbers increased by 33% to 311 (2023: 233)

· 37 fund finance mandates signed

· Average revenue per RM client decreased by 2% following significant increase in new clients, combined with continued macro headwinds

· Headcount increased to 267, 18% of which were Front Office (2023: 251, 14% of which were Front Office)

· Underlying profit before tax margin of 27% (2023: 32%)

About

Our Private Markets division, headquartered in the UK, and with operations in Luxembourg and Malta, is becoming a leading banking alternative for the private capital markets sector, covering: private equity, private credit, venture capital, real estate, infrastructure, and fund of funds.

Aligned with our high-tech, high-touch approach, we offer financial solutions, traditionally provided by banks, but designed to address the complexities and specific needs of private markets. Our services include:

- Accounts & Payments: simplified formation and management of accounts, coupled with efficient and reliable multi-currency payments with a global reach.

- Risk management: strategic advisory and execution services for managing currency exposures, with an emerging focus on interest rate risk management.

- Fund finance: streamlined debt-sourcing and expert advisory around the structuring of fund finance facilities.

Business Environment

The macroeconomic environment in 2024 remained challenging, with subdued deal and transaction volumes persisting across private markets. Data provider Preqin showed total deal value up 0.1% year-on-year, whilst deal volumes remained significantly below historic norms, largely due to relatively high interest rates. The growth in total deal value relative to deal volume reflects the fact that fewer but larger transactions are being made, highlighting a preference for larger investments in more established companies - known within the industry as 'mega-deals'.

In response, we expanded our focus upstream to encompass the larger end of the market. Whilst larger funds typically require a higher level of stature and financial standing from their suppliers, with our enhanced balance sheet and FTSE 250 reputation, this approach has begun to yield results, providing a foundation to pursue even more opportunities as macro conditions improve.

While we are not relying on any material change in the macro backdrop in 2025 to deliver on our ambitions, there is nonetheless an encouraging view within the market that we will see an increase in activity. Private equity firms face growing pressure to generate returns and exit long-held assets, as easing inflation and falling interest rates also drive an improvement in valuation multiples. As a result, more funds are expected to take advantage of acquisition opportunities and deploy new capital in 2025 than in previous years.2

Performance

Despite the challenging environment, 2024 was a year of very encouraging progress for Alpha's Private Markets division, with revenues increasing by 20% to £69m. Alpha's growing product portfolio, solid demand for these products, and the team's cross-selling capabilities are key drivers in this outperformance. A detailed breakdown of performance across our core offerings is provided below.

Risk Management (RM)

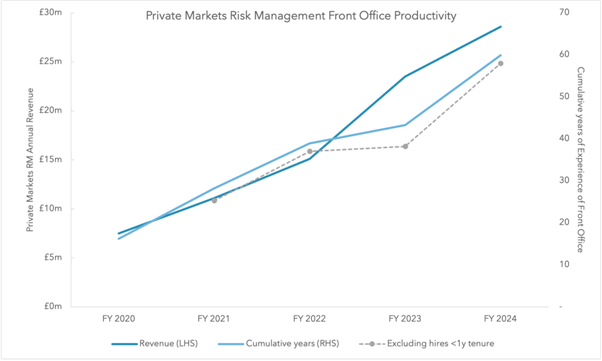

The Private Markets RM team delivered another strong performance. Revenue increased 20% in the period to £28.3m (FY 2023: £23.5m) with client numbers increasing 33% to 311 (December 2023: 233). This strong performance reflects the rewards of investing in our sales team, their high levels of productivity (see chart below), and our growing reputation, helped by the inclusion in the FTSE 250 and the expansion of our product offerings. In addition, we see continued success in the cross-selling between these product offerings, with accounts & payments, and fund finance facilitating introductions to our RM offering (and vice versa). Average revenue per client decreased by 2%, but this is a natural by-product of the record number of new clients we have onboarded, many of which are in the earlier stages of us growing wallet share. For context, client numbers increased by 33% from 233 to 311 between 2023 and 2024, whereas between 2022 and 2023 they increased by 10%, from 211 to 233.

The narrowing gap between revenue and cumulative years of front office experience reflects a small reduction in productivity in the year. This was not unexpected given private market deal volumes continued to decline across our core markets. As the market unwinds and our teams continue to mature and scale, we expect to see productivity increase, much like we have seen in our Corporate division.

Accounts & Payments (formerly alternative banking)3

Accounts & Payments revenues increased by 20% to £40.6m (FY 2023: £33.9m) and account numbers increased to 7,103 (2023: 6,467), despite the subdued levels of deal activity within the market and the knock-on effect this had on the need for accounts.

Our market outperformance reflects the investments in the efficiency and capabilities of our purpose-built technology, the increasing automation of sophisticated client onboarding, the growing penetration into larger asset managers, increasing levels of cross-selling between our products, and the expansion of our sales teams, which we began to build in 2023.

The interest rate environment contributed an additional £84m in net treasury income from client balances. This income stream serves as a natural hedge against the adverse impact that high interest rates have on private markets deal activity, which is the main factor impacting demand for our services. 2024 client balances averaged £2.15bn, which earned an average interest rate of 3.8% across the year, as the table below shows in more detail.

3 Our "alternative banking" product has been renamed to our "accounts & payments" product. We have changed this label as we believe that the whole of Alpha's offering can be categorised as a "banking alternative", whilst "accounts and payments" is a more specific description of the individual products being provided in this segment.

| Quarter | Blended average client balance, Accounts & Payments | Blended average interest rate |

| Q4 2024 | £2.3bn | 3.5% |

| Q3 2024 | £2.2bn | 3.8% |

| Q2 2024 | £2.1bn | 3.9% |

| Q1 2024 | £2.0bn | 4.0% |

| Q4 2023 | £2.1bn | 3.8% |

| Q3 2023 | £1.9bn | 3.8% |

| Q2 2023 | £1.9bn | 3.8% |

| Q1 2023 | £1.6bn | 2.8% |

We will continue to disclose this income stream separately from our underlying revenues, to reflect the fact that interest rates are a variable we cannot control. Nonetheless, as interest rates are likely to remain "higher-for-longer", this provides a significant income stream that we will continue to benefit from, particularly as the aggregate balances we hold for our clients are likely to continue to increase as the number of accounts grows. Alpha is able to obtain an attractive interest rate return on these client balances through our ability to aggregate numerous individual balances, most of which are transitory in nature and individually low in value. In addition to the interest income received on these balances, Alpha is investing in a new offering designed to allow customers to gain access to a wider variety of interest rate products in return for an arrangement fee.

The previous years' investments into the operational scalability of our accounts & payments offering continue to drive increasing levels of operational gearing. The number of accounts per staff member continues to increase, driven by increasing levels of automation and process optimisation.

Fund Finance

The Fund Finance team continues to make very pleasing progress in both adding new clients and winning increasingly larger-value mandates, which has resulted in revenues increasing by over 130% to £1.7m (2023: £0.7m). This is against the backdrop of a quiet market and highlights the quality of the team and the modular client proposition they have built, as well as the potential of the business as the market recovers.

Work is also underway to continue upgrading our digital debt-sourcing platform, Alpha Match. These upgrades will represent another industry-first within the private markets, and we look forward to providing more details once publicly launched.

Private Markets Growth Strategy

Alpha's Private Markets division has demonstrated impressive recent profit growth, supported by a favourable working capital profile, despite a period of low deal activity within its market. Given the investments we have made in people and technology over the last three years, we view the division as still very much in a build-out stage, highlighting the significant future opportunity, and potential operational gearing as the division scales. Although we place no reliance on it, any increase in deal activity in 2025 will naturally lead to more demand for our services. Beyond the anticipated market recovery, we have identified several long-term levers that can drive growth beyond volume increases.

First, alongside our channel partnerships with various service providers, there is significant potential to establish deeper, more direct client relationships with investment managers across all of our product lines. Historically, our direct interactions with investment managers have primarily focused on managing their FX exposures, with accounts & payments services largely managed through channel partners. By fostering more direct relationships across all of our product lines, we expect to enhance client loyalty, increase our stickiness, improve our ability to cross-sell, and expand our share of wallet.

Second, we see a potential long-term opportunity to extend our offering, in a measured way, beyond Europe, unlocking new markets and revenue streams in the US and Singapore. Many of our existing European clients already operate in these jurisdictions and have expressed an appetite for us to service their needs in North America and South East Asia, creating an exciting opportunity to quickly increase wallet share with firms that already know and trust us.

Finally, as we solidify our role as a trusted advisor to these fund clients, we have the chance to innovate and not only upgrade our existing solutions but also deliver new solutions in adjacent product areas that are cost-effective for Alpha to launch and support more of our clients' banking and financial risk management needs.

Cobase

Highlights (proforma)4

· Revenue growth of 70% to €3m (2023: €2m)

· Client numbers increased 59% to 214 (2023: 135)

· Annual recurring revenue ("ARR") at the end of the year at €5m

· Headcount remained at 21, with 6 Front Office and 15 Back Office (2023: 21)

4 Cobase was acquired on 1 December 2023, and during that month generated revenue of £0.2m, EBITDA of £0.0m, and a PBT loss of £0.2m, which was included in the Group's 2023 results.

Amsterdam-based Cobase is the Group's treasury-focused technology platform providing bank connectivity technologies that enable corporates and private market companies to manage all their banking relationships, accounts and transaction activity through one portal.

Operating under a SaaS-based subscription fee model with its own brand and team, Cobase has performed strongly during its first full year with the Group, following its acquisition in December 2023.

On a pro-forma basis, client numbers increased 59% to 214 (2023: 135), and revenues grew by 70% to €3m (2023: €2m), with increasing momentum seen in H2. During the year, Cobase achieved particular success with larger clients and saw some encouraging signs of cross-selling across our existing Corporate and Private Markets client base.

Cobase's simplicity of use, cost-effectiveness and ease of implementation, along with its flexible commercial terms with no onerous long-term contracts, represent a tangible competitive advantage in the treasury technology market. We have seen first-hand how CFOs and Treasurers managing multiple bank relationships value the ability to view and manage all their banking information and transactions in one place.

During the last year, the focus was allowing Cobase to optimise its treasury platform, over driving operational integration. We now feel the business is better prepared to work more closely with our Corporate and Private Markets teams to cross-sell to the Group's clients, as well as continuing to capture new clients of their own. This year we will therefore continue to invest in Cobase's existing sales teams, technology and integrations.

We expect further financial growth and increased client numbers in 2025 and, over the long term, expect this to deliver an increasingly meaningful contribution to Alpha as it integrates across the wider Group.

Capital Allocation and Share Buyback

The Group generated significant levels of cash in 2024. As at 31 December 2024 we had net assets of £279m (2023: £223m), with adjusted net cash increasing by c. £40m to £218m (2023: £179m).

We review our cash position on a regular basis, and if we feel our cash position becomes greater than we require, will look to reassess our capital allocation.

During the year, we were pleased to initiate two Share Buyback programmes, totalling £40m. The first £20m buyback programme was announced on 29 January and completed in full on 27 June. Our second buyback, announced on 1 May, commenced on 28 June. We have completed roughly half of this second buyback programme and expect it to conclude in the first half of 2025.

Our overarching preference remains to allocate capital into high-confidence organic growth initiatives, within both existing and potential new business units. Such initiatives include extending and improving product lines and tech solutions, expanding our territories when appropriate, or any other moat-widening opportunities that differentiate us from competitors. Although we are not actively seeking them out, we will consider complementary acquisitions that could further amplify revenue growth and enhance our proposition.

In view of the Group's confidence in the sizable and exciting market opportunities presented to us, the Board believes that, after maintaining our progressive dividend policy and executing value-capped share buybacks, retaining and deploying our remaining cash to grow the business will deliver the best value for shareholders long-term.

In addition to providing cash for investment, a strong balance sheet is also important to our counterparties. A healthy cash profile also provides our clients with confidence.

Chief Financial Officer's Report

Revenue

2024 has seen strong growth across both divisions despite a challenging macroeconomic environment, with total revenue increasing 23% to £136m (2022: £110m). Corporate revenue grew 21% to £63.8m (2023: £52.8m), and Private Markets (formerly "Institutional") grew 20% to £69.0m (2023: £57.4m). Cobase, the group's first acquisition, contributed £2.9m of revenue in its first full year of ownership.

Corporate

The Corporate division focuses on supporting corporates in managing their business risks associated with foreign currency, interest rates and, most recently, commodities, through the Group's sales teams located in London, Toronto, Amsterdam, Milan, Madrid, Munich, and Sydney. Revenue grew by 21% over the prior year to £63.8m (2023: £52.8m).

The UK office returned to growth in 2024 following an investment in rebuilding the talent and experience in the team, having been impacted by the necessary exporting of talent to launch the overseas offices in the prior year. UK revenue growth in 2024 was c. 7% year on year, with momentum building in the second half.

All overseas offices showed excellent YoY growth except Canada, which was flat. A new Canadian leadership team was installed in late 2023 and Canada has begun to see the benefits of this change in 2024, with revenue growing sequentially in H2 over H1, giving confidence that the right structure is in place to return to growth in 2025. The collective growth rate of Alpha's remaining overseas offices meanwhile was nearly 60%, highlighting the merit of the Group's global expansion strategy.

Overall the division saw strong underlying profit margin growth to c. 49% (2023: c. 47%).

Private Markets (formerly "Institutional")

Private Markets revenue grew 20% from £57.4m in the prior year to £69.0m in 2024, driven by an increased number of accounts, increased risk management revenue and a full year of revenue from our new Fund Finance offering which was launched in 2023.

Each of the division's core products showed strong growth despite the subdued levels of deal activity within the market:

· The Private Markets Risk Management team delivered another strong performance. Revenue increased 17% in the period, with client numbers increasing 33% to 311 (2023: 233).

· Accounts & Payments revenues increased by 20%, from £33.9m to £40.6m and account numbers increased to 7,103 (2023: 6,467). Revenue from annual account fees is recognised on a straight-line basis over the 12 months from the date the account was opened or renewed. At 31 December 2024 deferred revenue was £8.1m (2023: £7.1m), and this will be recognised as revenue in 2025.

· Fund finance continued its encouraging growth with over £1.7m of revenue in its first full year of operations (143% growth).

The underlying operating profit margin of the division was c. 27% (2023: c. 32%). The reduction against 2023 was predominately due to the timing mismatch of in-year investment, increased deferred account fees and the macro environment suppressing revenues.

Cobase

Momentum continues to build in Cobase following its acquisition in December 2023. Cobase operates a SaaS-based subscription fee model, and on a proforma basis, client numbers and revenue increased by 59% and 70% respectively in the year to 214 and €3m (2023: €2m). This growth in its first full year of ownership validates the acquisition rationale and supports confidence in Cobase's ability to make an increasingly meaningful contribution over time as it continues to integrate with the wider group.

Group Profitability

Statutory profit before tax increased by 6% to £123.1m (2023: £115.9m). Underlying profit is presented in the income statement to allow a better understanding of the Group's financial performance on a comparable basis from year to year. The underlying profit excludes the impact of the net treasury income on client balances (see below) and non-underlying items. On this basis, the underlying profit before tax increased by 10% to £47.4m (2023: £43.0m). The underlying organic profit before tax (excluding Cobase) growth was 15%.

As previously highlighted, the Group continued to invest in the year, specifically in the Private Markets division as we build out our products and offerings. Investments included a full year of the new Private Markets HQ in London, and further technology improvements to increase scalability and digitisation. Overall headcount increased in the year from 480 to over 524 at 31 December 2024 to support future long-term growth. Importantly, the ratio of front office versus back office staff has increased in both divisions, laying the foundations for future growth. The underlying profit before tax margin, excluding Cobase, reduced slightly to 37% (2023: 39%) due to us continuing to invest in long-term growth, and the suppressed macro environment. The statutory profit before tax margin remained high at 56% reflecting the net treasury income from client balances.

Net Treasury Income (NTI)

The current interest rate environment has allowed the Group to continue benefitting from interest income generated from client balances. 'Net treasury income - client funds' has contributed £84.0m of net treasury income in the year (2023: £73.7m), with the number and size of client balances growing to an average of £2.3bn in Q4 2024.

Whilst this interest income stream is a positive boost for the Group and a natural by-product of our increasingly diversified product offering, we are mindful that aspects of its dynamics are driven by macroeconomics beyond our control. As previously outlined, we recognise this income on client balances as 'net treasury income - client balances' and continue to exclude it from our underlying results.

The Group has also generated net treasury income on the initial and variation margins it requires for its Risk Management client relationships. These balances contribute to the Group's cash and cash equivalent balances and directly relate to the business's operating activities. Therefore, we have decided to separately disclose these amounts within total income at the top of the Income Statement, as opposed to within finance income, 2024: £1.3m (2023: £1.8m).

Taxation

The effective tax rate for the period was 24.7% (2023: 23.4%). The increase in effective rate is primarily due to the change in UK corporation tax from 19% to 25% in April 2023. The rate was lower than the pro rata UK headline rate of 25% due to the mix of profits across our global subsidiaries. There were no other material changes in underlying rates.

Earnings Per Share

Underlying basic earnings per share was up 13% at 86.4p (2023: 76.7p), whilst statutory basic earnings per share was up 5% at 215.7p (2023: 206.2p).

Key Performance Indicators

The Group monitors its performance using several key performance indicators which are reviewed at Executive Committee and Board level. The key financial performance indicators are revenue, total income, underlying profit before tax, profit before tax, PBT margin, adjusted free cash, number of Corporate clients, number of Private Markets Risk management clients, number of Accounts & Payments client accounts, and the front office to back office headcount ratios.

Cash Flow and Balance Sheet

In the year ended 31 December 2024, 53% of the revenue in the year was derived from products where the revenue is converted into cash within a few days of the trade date (2023: 53%). Including net treasury income, cash conversion was 72% in 2024 (2023: 72%). This has continued to have a positive impact on the Group's cash flow. On a statutory basis, net cash and cash equivalents increased in the year by £55m to £252.5m.

The Group's statutory cash position can fluctuate significantly from day to day due to the impact of changes in: collateral paid to banking partners, margin received from clients, early settlement of trades, or the unrealised mark-to-market profit or loss from client swaps. These movements result in an increase or decrease in cash with a corresponding change in other payables and trade receivables. Therefore, in addition to the statutory cash flow, the Group presents an adjusted net cash summary excluding these items, shown below. On this basis, adjusted net cash increased in the year by £39m to £217.5m.

| | 31 December | 31 December |

| | £'m | £'m |

| Net cash and cash equivalents | 252.5 | 197.9 |

| Variation margin (owed by)/paid to banking counterparties* | (13.1) | 11.1 |

| | 239.4 | 209.0 |

| Margin received from clients** | (35.3) | (51.1) |

| Net MTM timing of profit from client drawdowns and extensions within trade receivables |

13.4 |

20.9 |

| | | |

| Adjusted net cash*** | 217.5 | 178.8 |

*Includes MTM on Alpha's interest rate swaps

**Included in 'other payables' within 'trade and other payables'.

*** Excluding collateral received from clients, collateral paid to banking counterparties, early settlement of trades and the unrealised mark-to-market profit or loss from client swaps and rolls.

The overall net assets of the Group increased in the year by £56m to £279m (2023: £223m).

Buyback

During 2024 we announced two share buyback programmes of up to £20m. The first programme completed in June 2024. As at 31 December, £10m of the second programme had also been completed. As at 18 March 2025, a further £4m of the second programme had been completed.

Dividend

Following the strong full-year results, the Board is pleased to declare a final dividend of 14.0p per share (2023: 12.3p). Subject to shareholder approval, the final dividend will be payable to shareholders on the register at 25 April 2025, and will be paid on 23 May 2025. This represents a total dividend for the year of 18.2p per share (2023: 16.0p).

Despite having sufficient reserves across the Group, the Board recently became aware that the Company's reserves were insufficient, meaning certain dividends and share purchases were made other than in accordance with the Companies Act 2006. Details of the transactions which are affected by this issue (the "Relevant Purchases") are set out in Notes 14 and 17 to the Consolidated financial statements. Resolutions will be proposed to shareholders at the forthcoming AGM to remedy this matter.

Consolidated Statement of Comprehensive Income

For the year ended 31 December 2024

| | Year ended 31 December 2024 | Year ended 31 December 2023 | |

| | £'000 | £'000 | |

| | | | |

| REVENUE | 135,600 | 110,442 | |

| Net treasury income - client funds | 83,996 | 73,676 | |

| Net treasury income - own funds | 1,307 | 1,843 | |

| TOTAL INCOME | 220,903 | 185,961 | |

| Operating expenses | (102,608) | (73,809) | |

| OPERATING PROFIT | 118,295 | 112,152 | |

| Underlying operating profit | 42,556 | 39,205 | |

| Net treasury income - client funds | 83,996 | 73,676 | |

| Non-underlying items | (8,257) | (729) | |

| Finance income | 6,053 | 4,616 | |

| Finance expenses | (1,234) | (834) | |

| PROFIT BEFORE TAXATION | 123,114 | 115,934 | |

| Underlying profit before taxation | 47,375 | 42,987 | |

| Net treasury income - client funds | 83,996 | 73,676 | |

| Non-underlying items | (8,257) | (729) | |

| Taxation | (30,389) | (27,142) | |

| PROFIT FOR THE YEAR | 92,725 | 88,792 | |

| Attributable to: | | | |

| Equity holders of the parent | | 93,019 | 88,825 |

| Non-controlling interests | | (294) | (33) |

| PROFIT FOR THE YEAR | | 92,725 | 88,792 |

| OTHER COMPREHENSIVE INCOME/(LOSS): | | | |

| Items that will or may be reclassified to the profit or loss: | | | |

| Exchange loss on translation of foreign operations | | (2,485) | (679) |

| (Loss)/gain recognised on hedging instruments | | (1,318) | 3,193 |

| Tax relating to items that may be reclassified | | 329 | (798) |

| TOTAL COMPREHENSIVE INCOME FOR THE YEAR | | 89,251 | 90,508 |

| Attributable to: | | | |

| Equity holders of the parent | | 89,576 | 90,541 |

| Non-controlling interests | | (325) | (33) |

| TOTAL COMPREHENSIVE INCOME FOR THE YEAR | | 89,251 | 90,508 |

|

Earnings per share (EPS) attributable to equity owners of the Parent (pence per share) | |||

| - basic | 215.7p | 206.2p | |

| - diluted | 211.7p | 203.4p | |

| - underlying basic | 86.4p | 76.7p | |

| - underlying diluted | 84.8p | 75.6p | |

Consolidated Statement of Financial Position

| As at 31 December 2024 | Company number: 07262416 |

| |||

|

|

| As at 31 December 2024 | As at 31 December 2023 | ||

|

|

| | Restated1 | ||

| NON-CURRENT ASSETS | £'000 | £'000 | |||

| Goodwill | 4,526 | 4,707 | |||

| Intangible assets | 14,957 | 14,007 | |||

| Property, plant and equipment | 7,670 | 8,800 | |||

| Right-of-use assets | 18,993 | 20,894 | |||

| Derivative financial assets | 28,699 | 14,369 | |||

| TOTAL NON-CURRENT ASSETS | 74,845 | 62,777 | |||

| CURRENT ASSETS | | | |||

| Cash and cash equivalents | 252,468 | 197,941 | |||

| Derivative financial assets | 132,446 | 90,966 | |||

| Trade and other receivables | 12,715 | 12,033 | |||

| Fixed collateral | 10,063 | 8,810 | |||

| Current tax asset | - | 73 | |||

| TOTAL CURRENT ASSETS | 407,692 | 309,823 | |||

| TOTAL ASSETS | 482,537 | 372,600 | |||

|

EQUITY | | | |||

| Share capital | 87 | 87 | |||

| Share premium account | 52,566 | 52,566 | |||

| Treasury shares | (6,697) | - | |||

| Retained earnings | 235,256 | 170,939 | |||

| Other reserves | (3,086) | (632) | |||

| EQUITY ATTRIBUTABLE TO EQUITY HOLDERS OF THE PARENT | 278,126 | 222,960 | |||

| Non-controlling interests | 879 | 531 | |||

| TOTAL EQUITY | 279,005 | 223,491 | |||

| CURRENT LIABILITIES | | | |||

| Derivative financial liabilities | 84,080 | 34,288 | |||

| Other payables | 45,747 | 59,750 | |||

| Deferred income | 8,059 | 7,072 | |||

| Lease liability | 2,180 | 1,028 | |||

| Current tax liability | 12,086 | 11,293 | |||

| TOTAL CURRENT LIABILITIES | 152,152 | 113,431 | |||

| NON-CURRENT LIABILITIES | | | |||

| Derivative financial liabilities | 24,695 | 5,922 | |||

| Other payables | 885 | 875 | |||

| Redemption liability | 1,812 | 1,884 | |||

| Deferred tax liability | 3,661 | 5,305 | |||

| Lease liability | 20,327 | 21,692 | |||

| TOTAL NON-CURRENT LIABILITIES | 51,380 | 35,678 | |||

| TOTAL LIABILITIES | 203,532 | 149,109 | |||

| TOTAL EQUITY AND LIABILITIES | 482,537 | 372,600 | |||

The Consolidated Financial Statements of Alpha Group International plc were approved by the Board of Directors on 18 March 2025 and signed on its behalf by:

C Kahn, Director T Powell, Director

[1] See note 12 for details of the prior year restatement.

Consolidated Statement of Cash Flows

For the year ended 31 December 2024

| | Year ended 31 December 2024 | Year ended 31 December 2023 | |

| | | Restated2 | |

| CASH FLOWS FROM OPERATING ACTIVITIES | £'000 | £'000 | |

| Profit before taxation | 123,114 | 115,934 | |

| Net treasury income - client funds | (83,996) | (73,676) | |

| Net treasury income - own funds | (1,307) | (1,843) | |

| Finance income | (6,053) | (4,616) | |

| Finance expense | 1,234 | 834 | |

| Amortisation and impairment of intangible assets | 6,598 | 3,137 | |

| Depreciation of property, plant and equipment | 1,782 | 1,325 | |

| Depreciation of right-of-use assets | 2,793 | 1,939 | |

| Loss on disposal of property, plant and equipment | 224 | 8 | |

| Gain on disposal of right-of-use asset | (93) | - | |

| Share-based payment expense/(credit) | 5,325 | (58) | |

| Increase in other receivables | (752) | (3,858) | |

| Decrease in other payables | (13,670) | (15,550) | |

| (Increase)/decrease in derivative financial assets | (53,712) | 22,435 | |

| Increase/(decrease) in derivative financial liabilities | 65,149 | (9,232) | |

| Increase in fixed collateral | (1,253) | (4,084) | |

| CASH INFLOWS FROM OPERATING ACTIVITIES | 45,383 | 32,695 | |

| Net treasury income received | 85,598 | 73,975 | |

| Tax paid | (30,451) | (15,881) | |

| NET CASH INFLOWS FROM OPERATING ACTIVITIES | 100,530 | 90,789 | |

| CASH FLOWS FROM INVESTING ACTIVITIES | | | |

| Acquisition of subsidiary, net of cash acquired | - | (8,227) | |

| Payments to acquire property, plant and equipment | (1,038) | (6,927) | |

| Payments to acquire right-of-use assets

| (25) | (235) | |

| Proceeds from the disposal of right-of-use assets | 20 | - | |

| Proceeds from sale of property, plant and equipment | 4 | 5 | |

| Expenditure on intangible assets | (7,739) | (8,025) | |

| Finance income received | 6,053 | 4,616 | |

| NET CASH OUTFLOWS FROM INVESTING ACTIVITIES | (2,725) | (18,793) | |

| CASH FLOWS FROM FINANCING ACTIVITIES | | | |

| Issue of ordinary shares by Parent Company | - | 491 | |

| Issue of treasury shares by Parent Company | 303 | - | |

| Purchase of own shares | (30,004) | - | |

| Acquisition of non-controlling interest | (48) | - | |

| Issue of share options | 26 | - | |

| Dividends paid to equity holders of Parent Company | (7,084) | (6,368) | |

| Dividends paid to subsidiary shareholders | (2,229) | (2,762) | |

| Payment of lease liabilities - principal | (1,065) | (779) | |

| Payment of lease liabilities - interest | (1,145) | (793) | |

| NET CASH OUTFLOWS FROM FINANCING ACTIVITIES | (41,246) | (10,211) | |

|

| | | |

| INCREASE IN NET CASH AND CASH EQUIVALENTS IN THE YEAR | 56,559 | 61,785 | |

| Net cash and cash equivalents at beginning of year | 197,941 | 136,799 | |

| Net exchange loss | (2,032) | (643) | |

| NET CASH AND CASH EQUIVALENTS AT END OF YEAR | 252,468 | 197,941 |

2 Prior year has been restated for the balance sheet reclassification outlined in note 12.

Consolidated Statement of Changes in Equity

For the year ended 31 December 2024

|

| ||||||||||

| | Share capital | Share premium account | Treasury shares | Retained earnings | Other reserves | Total | Non- controlling interests | Total | ||

|

| £'000 | £'000 | £'000 | £'000 | £'000 | £'000 | £'000 | £'000 | ||

| Balance at 1 January 2023 | 84 | 52,075 | - | 88,807 | 1,931 | 142,897 | - | 142,897 | ||

| Profit/(loss) for the year | - | - | - | 88,825 | - | 88,825 | (33) |

| 88,792 | |

| Other comprehensive income/(expense): |

|

| ||||||||

| Gains recognised on hedging instruments | - | - | - | 2,395 | - | 2,395 | - | 2,395 | ||

| Exchange differences arising on translation of foreign operations | - | - | - | - | (679) | (679) | - | (679) | ||

| Transactions with owners: | | | |

| | | | | ||

| Acquisition of subsidiary | - | - | - | 103 | (1,884) | (1,781) | 564 | (1,217) | ||

| Shares issued on vesting of share option schemes | 3 | 491 | - | (3) | - | 491 | - | 491 | ||

| Share-based payments | - | - | - | (58) | - | (58) | - | (58) | ||

| Dividends paid (note 9) | - | - | - | (9,130) | - | (9,130) | - | (9,130) | ||

| Balance at 31 December 2023 | 87 | 52,566 | - | 170,939 | (632) | 222,960 | 531 | 223,491 | ||

| Profit/(loss) for the year | - | - | | 93,019 | | 93,019 | (294) | | 92,725 | |

| Other comprehensive expense: | | |||||||||

| Losses recognised on hedging instruments | - | - | - | (989) | - | (989) | - | (989) | ||

| Exchange differences arising on translation of foreign operations | - | - | - | - | (2,454) | (2,454) | (31) | (2,485) | ||

| Transactions with owners: | | | | | | | | | ||

| Capital contribution to subsidiary with minority interest | - | - | - | (676) | - | (676) | 676 | - | ||

| Acquisition of non-controlling interest | - | - | - | (45) | - | (45) | (3) | (48) | ||

| Acquisition of treasury shares (note 14) | - | - | (10,721) | (19,283) | - | (30,004) | - | (30,004) | ||

| Treasury shares issued in relation to subsidiary earnout (note 14) | - | - | 4,024 | - | - | 4,024 | - | 4,024 | ||

| Issue of share options in subsidiary undertakings | - | - | - | (3,721) | - | (3,721) | - | (3,721) | ||

| Share-based payments | - | - | - | 5,325 | - | 5,325 | - | 5,325 | ||

| Dividends paid (note 9) | - | - | - | (9,313) | - | (9,313) | - | (9,313) | ||

| Balance at 31 December 2024 | 87 | 52,566 | (6,697) | 235,256 | (3,086) | 278,126 | 879 |

| 279,005 | |

Notes to the Consolidated Financial Statements

For the year ended 31 December 2024

1. General information

Alpha Group International plc (the "Company") is a public limited company, with ordinary shares on the Main Market of The London Stock Exchange since 2 May 2024 (previously listed on AIM, since 7 April 2017). The Company is incorporated and domiciled in the UK (registered number 07262416) and its registered office is Brunel Building, 2 Canalside Walk, London, England, W2 1DG.

Statutory accounts for the year ended 31 December 2023 have been delivered to the Registrar of Companies. The statutory accounts for the year ended 31 December 2024 will be delivered to the Registrar of Companies following the Group's Annual General Meeting.

The auditors' reports on the financial statements for 31 December 2023 and 31 December 2022 were unqualified, did not draw attention to any matters by way of emphasis, and did not contain a statement under 498(2) or 498(3) of the Companies Act 2006.

2. Material accounting policies

Basis of preparation

The Consolidated Financial Statements have been prepared in accordance with UK adopted international accounting standards using the measurement bases specified by UK IFRS for each type of asset, liability, revenue or expense.

The financial information set out above does not constitute statutory accounts for the purposes of section 435 of the Companies Act 2006, for the years ended 31 December 2024 and 31 December 2023, but is derived from those accounts.

The Directors have assessed the Group's projected business activities and available financial resources together with detailed forecasts for cash flow and relevant sensitivity analysis. The directors believe that the Group remains well placed to manage its business risks successfully. After making appropriate enquiries the directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. Accordingly, the directors continue to adopt the going concern basis in preparing the statutory accounts for the year ended 31 December 2024.

The preparation of consolidated financial statements in conformity with UK adopted IFRS requires management to make judgements, estimates and assumptions that affect the application of policies and reported amounts of assets, liabilities, income and expenses. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making judgements about the carrying value of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates.

3. Alternative performance measures

The Group uses alternative performance measures to monitor financial performance and cash flows (we refer to these results as 'adjusted' or 'underlying'). This is consistent with the way that financial performance is measured by management and reported to the Executive Committee and Board. These measures are not measures of performance under IFRS and should be considered in addition to, and not as a substitute for, IFRS measures of financial performance and liquidity. These measures may not be comparable across companies.

Financial performance

This note analyses non-underlying items, which are included in our results for the year but are excluded from underlying operating profit, underlying Profit before taxation and underlying EPS.

Non-underlying items in the year are made up of the below charges/ (credits):

| |

31 December 2024 |

31 December 2023 |

| | £'000 | £'000 |

| Acquisition costs in relation to business combinations | 104 | 487 |

| Other M&A related integration and transaction costs | 62 | |

| Costs associated with the move from AIM to the Main Market | 2,746 | 248 |

| Amortisation of purchased intangible assets | 82 | (10) |

| Share-based payments charge/(credit) | 5,325 | (58) |

| Total non-underlying items | 8,257 | 729 |

Share based payments and amortisation of intangible assets are non-cash underlying items, the cash flow impact of the other non-underlying items is not materially different from their impact on the Consolidated Statement of Comprehensive Income.

The following tables show the reconciliation of the Group's statutory financial performance measures to our underlying financial performance measures:

| | Operating profit | Profit before tax | Profit after tax | Earnings attributable to equity holders | Basic EPS |

| Year ended 31 December 2024 | £'000 | £'000 | £'000 | £'000 | Pence |

| Statutory measure | 118,295 | 123,114 | 92,725 | 93,019 | 215.7 |

| | | | | | |

| (Deduct)/add back: | | | | | |

| NTI - client funds | (83,996) | (83,996) | (83,996) | (83,996) | (194.8) |

| Non-underlying items | 8,257 | 8,257 | 8,257 | 8,257 | 19.2 |

| Tax effect of above items* | - | - | 19,971 | 19,971 | 46.3 |

| Underlying measure | 42,556 | 47,375 | 36,957 | 37,251 | 86.4 |

\* The tax effect includes £20,999k on the NTI client funds, £876k of allowable share-based payment charges across the Group and £152k of allowable costs associated with the move from AIM to the Main Market.

3. Alternative performance measures (continued)

| | Operating profit | Profit before tax | Profit after tax | Earnings attributable to equity holders | Basic EPS |

| Year ended 31 December 2023 | £'000 | £'000 | £'000 | £'000 | Pence |

| Statutory measure | 112,152 | 115,934 | 88,792 | 88,825 | 206.2 |

| | | | | | |

| (Deduct)/add back: | | | | | |

| NTI - client funds | (73,676) | (73,676) | (73,676) | (73,676) | (171.0) |

| Non-underlying items | 729 | 729 | 729 | 729 | 1.7 |

| Tax effect of above items | - | - | 17,143 | 17,143 | 39.8 |

| | | | |||

| Underlying measure | 39,205 | 42,987 | 32,988 | 33,021 | 76.7 |

Cash flows

The Group's statutory cash position can fluctuate significantly from day to day due to the impact of changes in: collateral paid to banking partners, margin received from clients, early settlement of trades, or the unrealised mark-to-market profit or loss from client swaps. These movements result in an increase or decrease in cash with a corresponding change in other payables and trade receivables. Therefore, in addition to the statutory cash flow, the Group presents an adjusted net cash summary excluding these items, shown below. On this basis, adjusted net cash increased in the year by £39m to £217.5m.

| |

31 December 2024 |

31 December 2023 |

| | £'000 | £'000 |

| Statutory cash and cash equivalents | 252,468 | 197,941 |

| Variation margin (receivable from)/paid to banking counterparties* | (13,097) | 11,125 |

| | 239,371 | 209,066 |

| Margin received from clients** | (35,336) | (51,137) |

| Net MTM timing of profit from client drawdowns and extensions within trade receivables | 13,503 | 20,897 |

| Adjusted net cash*** | 217,538 | 178,826 |

*Includes MTM on Alpha's interest rate swaps

** Included in 'other payables' within 'trade and other payables'.

*** Excluding collateral received from clients, collateral paid to banking counterparties, early settlement of trades and the unrealised mark to market profit or loss from client swaps and rolls.

4. Segmental reporting

During the year the Group has evolved its organisational structure from a product centric structure to a client centric structure and as a result this structure has been mirrored within the presentation of the financial statements in accordance with IFRS. The Group now comprises three operating segments which are Corporate, Private Markets* and Cobase. These align with the management accountabilities for performance management and the basis for internal financial reporting and represent our reportable segments. These three segments are explained further as below:

· Corporate focuses on currency risk management to corporate clients, primarily for the purpose of hedging commercial foreign exchange exposures.

· Private Markets includes accounts & payments- simplified formation and management of currency accounts, coupled with efficient and reliable multi-currency payments across key investment jurisdictions. Currency management: strategic advisory and execution services for managing currency exposures, with a growing focus on interest rate risk management and Fund finance: streamlined debt-sourcing and expert advisory around the structuring of facilities.

· Cobase, a Dutch based company that was acquired by the Group in December 2023. Cobase is a cloud-based provider of bank connectivity technology that enables corporates to manage their banking relationships and transactions.

*As described further in the Chief Executive's Statement, the Institutional division has been renamed to "Private Capital Markets" or "Private Markets" for short. This change has been made as it is a clearer description of the types of clients that Alpha service.

The chief operating decision makers, being the Group's Chief Executive Officer and the Chief Financial Officer, monitor the results of the three operating segments separately each month. Key measures of operating segments used to evaluate performance are revenue, and underlying profit before taxation. Management believe that these measures are the most relevant in evaluating the performance of the segment and for making resource allocation decisions.

The Group has disclosed revenue for each segment disaggregated between Risk Management, Accounts & payments and platform fees, to assist users in understanding the product mix. All costs are attributed to these segments.

As explained further in note 3, the Group excludes 'Net treasury income - client funds' from the definition of underlying profit. 'Net treasury income - own funds' relates to interest earned on client margin held by the Corporate division and is incorporated in the definition of underlying profit for that business as this income is a direct consequence of operational activities.

The Corporate division has overseas offices in Australia, Canada, Netherlands, Italy, Spain and Germany. In 2024, these offices contributed aggregate revenue of £27.2m and underlying profit before taxation of £6.6m (£18.7m and £3.8m underlying profit respectively in prior year). A small component of Private Markets costs arise in Luxembourg, and the profit related to the Malta office has been allocated between the various European entities it supports.

4. Segmental reporting (continued)

| 2024 |

Corporate |

Private Markets |

Cobase |

Total |

| | £'000 | £'000 | £'000 | £'000 |

| Risk Management* | 63,759 | 28,344 | - | 92,103 |

| Accounts & payments** Platform fees | - - | 40,610 - | - 2,887 | 40,610 2,887 |

| Total revenue | 63,759 | 68,954 | 2,887 | 135,600 |

| Net treasury income - own funds Segment income | 1,307 65,066 | - 68,954 | - 2,887 | 1,307 136,907 |

| Operating costs*** | (39,261) | (49,893) | (5,197) | (94,351) |

| | | | | |

| Underlying operating profit | 25,805 | 19,061 | (2,310) | 42,556 |

|

Finance Income Finance expense |

6,016 (457) |

37 (777) |

- - |

6,053 (1,234) |

| Underlying profit before taxation | 31,364 | 18,321 | (2,310) | 47,375 |

|

Net treasury income - client funds |

4,059 |

79,937 |

- |

83,996

|

| Non-underlying items | | | | (8,257) |

| Profit before taxation | | | | 123,114 |

| 2023 Re-presented |

Corporate |

Private Markets |

Cobase |

Total |

| | £'000 | £'000 | £'000 | £'000 |

| Risk Management* | 52,811 | 23,518 | - | 76,329 |

| Accounts & payments** Platform fees | - - | 33,927 - | - 186 | 33,927 186 |

| Total revenue | 52,811 | 57,445 | 186 | 110,442 |

| Net treasury income - own funds Segment income | 1,843 54,654 | - 57,445 | - 186 | 1,843 112,285 |

| Operating costs*** | (34,060) | (38,586) | (434) | (73,080) |

| | | | | |

| Underlying operating profit | 20,594 | 18,859 | (248) | 39,205 |

| | | | | |

| Finance Income Finance expense | 4,611 (399) | - (435) | 5 - | 4,616 (834) |

| Underlying profit before taxation | 24,806 | 18,424 | (243) | 42,987 |

|

Net treasury income - client funds

Non-underlying items |

5,534

|

68,142

|

-

|

73,676

(729) |

| Profit before taxation | | | | 115,934 |

4. Segmental reporting (continued)

*Risk Management represents revenue derived from forward, spot, and option contracts provided to corporate and private market clients, primarily for the purpose of hedging commercial foreign exchange exposures.

**Accounts & payments represents revenues derived from fees and foreign exchange spot contracts

generated from the provision of cross border payments, collections and annual account fees to corporates and private markets, as well as Fund Finance advisory fees.

***Operating costs excludes non-underlying items as set out in Note 4 above.

All revenue is from external customers and is based on the location of those customers.

| Revenue by region of customer | 31 December 2024 £'000 | 31 December 2023 £'000 |

| United Kingdom | 43,578 | 40,252 |

| Europe | 68,847 | 55,238 |

| Canada | 4,389 | 4,251 |

| Rest of the world | 18,786 | 10,701 |

| Total | 135,600 | 110,442 |

No customer represents more than 10% of revenue and the Group does not believe there is undue reliance on any specific sub-set of customers.

| Revenue by product

| | 31 December 2024 £'000 | 31 December 2023 £'000 |

| Forward transactions Spot transactions Option contracts Payments, accounts and advisory fees Platform fees | | 63,268 32,590 11,650 25,205 2,887 | 51,966 31,791 7,823 18,676 186 |

| Total |

| 135,600 | 110,442 |

|

|

|

|

|

Forward, spot and option revenues are accounted for under IFRS 9 - Financial Instruments, and the remaining revenue streams i.e. payments, accounts, advisory and platform fees fall under IFRS 15 - Revenue from Contracts with Customers.

The table below discloses non-current assets (excluding financial instruments and deferred tax) by location:

|

Non-current assets

| 31 December 2024 £'000 | 31 December 2023 £'000 Re-presented* |

| United Kingdom | 26,879 | 29,911 |

| Malta | 6,068 | 5,287 |

| The Netherlands | 10,454 | 11,855 |

| Canada | 1,032 | 1,336 |

| Other | 1,713 | 19 |

| Total non-current assets | 46,146 | 48,408 |

4. Segmental reporting (continued)

* The 2023 prior year re-presentation relates to the exclusion of derivative financial assets which has been disclosed separately in line with IFRS 9 (see note 11).

No information is provided for segment assets or segment liabilities as this measure is not reported to the chief operating decision makers.

5. Operating profit

Operating profit is stated after charging/(crediting):

| | 31 December 2024 | 31 December 2023 |

| | £'000 | £'000 |

| Staff costs | 56,596 | 37,665 |

| Depreciation of owned property, plant and equipment | 1,782 | 1,325 |

| Amortisation of intangible assets* | 6,595 | 3,111 |

| Depreciation of right-of-use assets | 2,793 | 1,939 |

| Rental costs for short-term leases | 1,022 | 897 |

| Loss on disposal of fixed assets | 224 | 8 |

| Gain on disposal of right-of-use asset | (93) | - |

| Impairment of intangible assets | 3 | 26 |

| Bad debt expense | 508 | 135 |

| Net foreign exchange (gains)/losses | (409) | 372 |

| Audit fees | | |

| Audit fees in respect of the Group, Company and subsidiary financial statements |

896 | 758 |

| Non-Audit fees | | |

| Fees in respect of CASS Limited Assurance | 10 | 10 |

| Fees associated with the move from AIM to the Main Market | 498 | - |

*Amortisation of intangible assets includes a charge of £6,513k (2023: charge of £3,121k) relating to internally generated software and a charge of £82k (2023: credit of £10k) relating to brand and customer relationships.

6. Finance income and expenses

| | 31 December 2024 | 31 December 2023 |

| | £'000 | £'000 |

| Finance income | |

|

| Interest on bank deposits | 5,945 | 4,491 |

| Other interest receivable | 108 | 125 |

| Total | 6,053 | 4,616 |

|

| |

|

| Finance expenses | |

|

| Finance expense on dilapidation provisions | (34) | (41) |

| Finance expense on lease liabilities (note 10) | (1,200) | (793) |

| Total | (1,234) | (834) |

7. Taxation

Tax charge

| | 31 December 2024 | 31 December 2023 |

| | ||

| | £'000 | £'000 |

| Current tax: | | |

| UK Corporation tax on the profit for the year | 31,172 | 24,536 |

| Adjustments relating to prior years | (215) | (633) |

| Overseas corporation tax on the profit for the year | 744 | 219 |

| Total current tax | 31,701 | 24,122 |

|

| | |

| Deferred tax | | |

| Origination and reversal of temporary differences current year | (427) | 3,020 |

| Adjustment relating to prior year | (885) | - |

| Total deferred tax | (1,312) | 3,020 |

| | | |

| Total tax expense | 30,389 | 27,142 |

Deferred tax has decreased due to the comparatively high level of prior year investments in assets and the acquisition of Cobase.

Factors affecting tax charge for the year

| | 31 December 2024 | 31 December 2023 |

| | £'000 | £'000 |

| Profit on ordinary activities before tax | 123,114 | 115,934 |

| Profit on ordinary activities multiplied by the effective standard rate of UK corporation tax of 25% (2023: 23.5%) | 30,779 | 27,244 |

| Effects of: | | |

| Expenses not deductible for tax purposes | 610 | 561 |

| Unutilised trading losses different tax rates applied in overseas jurisdictions | 44 | 93 |

| Adjustments relating to prior years | (1,101) | (633) |

| Deferred tax not recognised on losses unutilised | 57 | - |

| Unutilised trading losses | - | (102) |

| Trading losses brought forward | - | (21) |

| Total tax charge for the year | 30,389 | 27,142 |

| | | |

7. Taxation (continued)

Factors affecting tax charge for the year (continued)

During the year, management identified that a £1.1m deferred tax liability recognised at 31 December 2023 in relation to the Cobase business had been overstated and the charge has been corrected in the current year. In addition, the Group has recognised a deferred tax asset of £0.4m in respect of future tax deductions for the amortisation of customer lists in Malta. This asset is expected to be amortised over the next two years.

Deferred tax

The deferred taxation liability is based on the expected future rate of corporation tax of 25% (2023: 25%) and comprises the following:

| | 31 December 2024 | 31 December 2023 |

| | £'000 | £'000 |

| Liabilities

| | |

| At 1 January | 5,305 | 1,387 |

| UK & overseas tax charge relating to current year from continuing operations | (343) | 1,960 |

| UK tax charge relating to current year from acquired operations | (971) | 1,060 |

| Fair market value at acquisition | - | 102 |

| Tax credit relating to foreign exchange rate movements | - | (2) |

| Tax (credit)/charge on other comprehensive income | (330) | 798 |

| Total deferred tax liability | 3,661 | 5,305 |

The UK deferred tax liability as at 31 December 2024 and as at 31 December 2023 principally relates to the tax effect of timing differences in respect of fixed assets.

Deferred tax - balance

| | 31 December 2024 | 31 December 2023 |

| | £'000 | £'000 |

| Liabilities

| | |

| Fixed asset differences | 3,890 | 4,564 |

| Fair market value at acquisition | - | 102 |

| Right-of-use assets | 2 | - |

| Losses | (115) | - |

| Foreign exchange rate movements | - | 1 |

| Future tax deductions for amortisation of customer lists in Malta | (405) | - |

| Gain recognised on hedging instruments | 289 | 638 |

| Total deferred tax liability | 3,661 | 5,305 |

| | | |

Losses of €28m (tax effect €4.4m) arose for periods prior the 2023 acquisition of Financial Transaction Services B.V. (Cobase). Under Dutch tax regulations these losses can be carried forward indefinitely but are only available for offset against a limited portion of profits in any given year. Based on the latest forecasts, no material losses are expected to be utilised in the near term and accordingly no deferred tax asset has been recognised. Losses in other jurisdictions carried forward for which no deferred tax asset has been recognised total £0.14m.

7. Taxation (continued)

Deferred tax on each component of other comprehensive income/(expense) is as follows:

| | |||||||

| Before tax | Tax | After tax | Before tax | Tax | After tax | ||

| | £'000 | £'000 | £'000 | £'000 | £'000 | £'000 | |

| Cash flow hedges |

| | | | | | |

| (Losses)/gains recognised on hedging instruments | (1,318) | 329 | (989) | 3,193 | (798) | 2,395 | |

| | | | | | | | |

| Exchange loss arising on translation of foreign operations | (2,485) | - | (2,485) | (679) | - | (679) | |

| Total tax (charge)/credit on other comprehensive income/(expense) | (3,803) | 329 | (3,474) | 2,514 | (798) | 1,716 | |

8. Earnings per share

Basic earnings per share is calculated by dividing the profit for the year attributable to equity holders of the Parent, by the weighted average number of ordinary shares in issue during the financial year. Diluted earnings per share additionally includes in the calculation, the weighted average number of ordinary shares that would be issued on conversion of any dilutive potential ordinary shares. The dilutive effect is calculated on the full exercise of all potentially dilutive ordinary share options granted by the Group.

The underlying calculation excludes the impact of net treasury income on client funds and other non-underlying items and their tax effect. This better enables comparison of financial performance in the current year with comparative years.

|

| 31 December 2024 | 31 December 2023 |

|

| Pence | Pence |

| Basic earnings per share | 215.7p | 206.2p |

| Diluted earnings per share | 211.7p | 203.4p |

| Underlying - basic | 86.4p | 76.7p |

| Underlying - diluted | 84.8p | 75.6p |

8. Earnings per share (continued)

The calculation of basic and diluted earnings per share is based on the following number of shares:

|

| 31 December 2024 | 31 December 2023 |

|

| No. | No. |

| Basic weighted average shares | 43,119,507 | 43,072,098 |

| Contingently issuable shares | 818,677 | 593,955 |

| Diluted weighted average shares | 43,938,184 | 43,666,053 |

The number of shares which are contingently issuable in respect of a number of employee incentive schemes will be determined based on the change in market capitalisation of the Group over a 60 business-day period running from 20 December 2024 to 18 March 2025. For the purposes of diluted EPS shown above the figure has been determined as if the market condition was finalised at the balance sheet date i.e. it has been based on the change in market capitalisation between 20 December 2024 and 31 December 2024.

As set out in note 14, £19.3m of purchases of shares by the Company during the year, and a further £3.5m post year end had been made otherwise than in accordance with the Companies Act 2006. The basic and diluted weighted average number of shares in issue shown above excludes these purchases. Had these been made in accordance with the legal requirements, the basic weighted average number of shares would have been 470,609 lower.

As at market close on 18 March 2025, excluding these purchases, the Group had 42,976,487 shares in issue. Had all purchases of shares been in accordance with the Act, this figure would have been 1,063,556 lower, or 41,912,931.

9. Dividends

|

| 31 December 2024 | 31 December 2023 |

|

| £'000 | £'000 |

| Final Plc dividend for the year ended 31 December 2022 of 11.0p per share | - | 4,765 |

| Interim Plc dividend for the year ended 31 December 2023 of 3.7p per share | - | 1,603 |

| Final Plc dividend for the year ended 31 December 2023 of 12.3p per share | 5,308 | - |

| Interim Plc dividend for the year ended 31 December 2024 of 4.2p per share | 1,776 | - |